Are the financial tremors over? Based on the latest data published by the Federal Reserve Bank of St. Louis (see graph below), it seems that we are returning to some normalcy. However, if the commercial real estate sector in the US and/or Europe starts its own series of tremors in the next 12-24 months (the probability is not low), then we should expect significant financial turmoil.

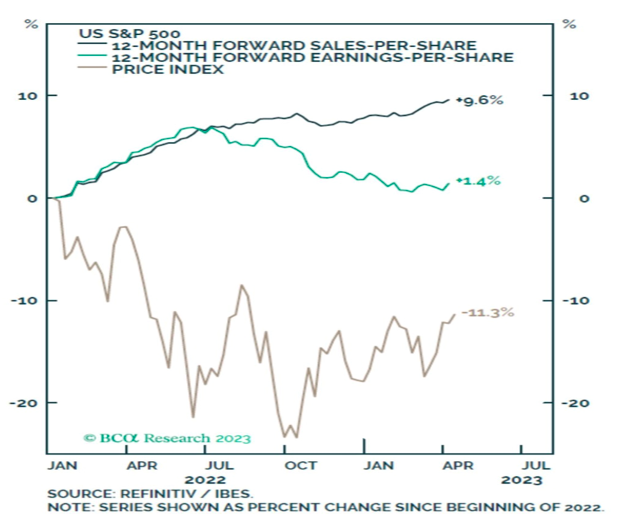

Given the equity markets’ recovery since the banking tremors, could we expect the stock market to continue its upswing? We would recommend caution. The figure below shows discrepancies. Specifically, since early 2022, sales per share are rising at a rate close to 10%, but those higher sales do not translate into earnings growth. Earnings growth is below 1.5%, which is very low and implies low equity premium. Consequently, the equity index has dropped by about 11%.

The equity premium (the extra yield of owing stocks vs. 10-year Treasuries) nowadays is around 1.60%, which is the lowest premium for the last fifteen years, while the S&P 500 index is still pricey relative to inflation-adjusted earnings (CAPE ratio). No wonder then, that the safety of Treasuries is more attractive than the expectation of stocks’ returns, as the probability of recession increased in the last few weeks.

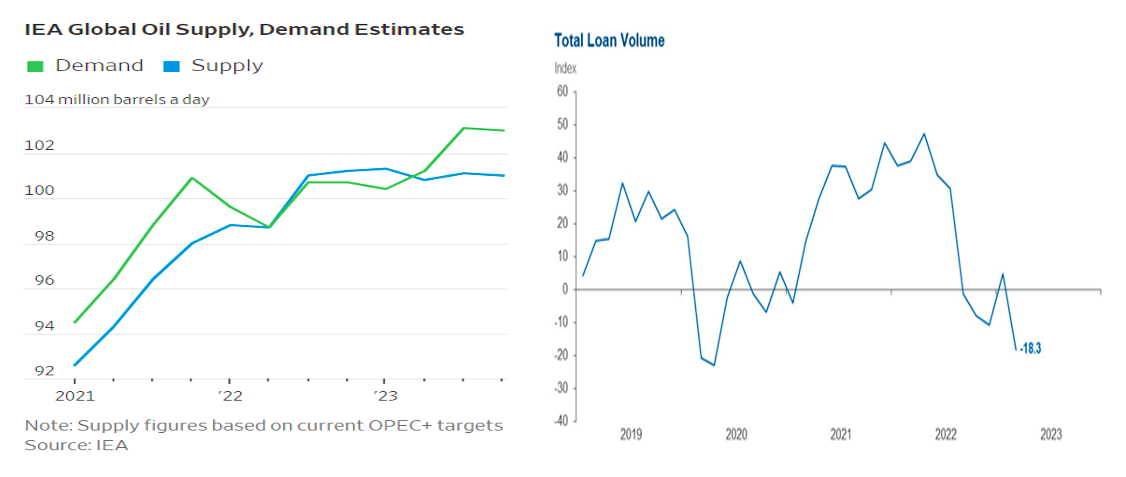

Recession fears are rising due to four reasons: First consumers’ spending shows clear signs of declining; second, corporate spending follows the same trend; third, credit conditions are tightening as reported by the Dallas Fed (see below); and finally, the combination of economic (growth slowdown, oil market deficits where demand exceeds supply, see graph below) and financial (inflation and interest rates) developments, allow the continuous inversion of the yield curve which in turn spells pessimism (even restrained) and tends to become a self-fulfilling prophecy.

It might be wise to be aware of the narrow choices we are facing no matter how vast the landscape may be. The dealer of the market’s fate cautions us to adopt that anxious foresight that can guard us against hubris. The merging of the heroic and tragedy’s grief helps us strive against insurmountable illusionary forces. In an era where technology may be opening unfathomable possibilities, learning the value of pain enables us to listen to the Chorus of Hebrew slaves in Verdi’s Nabucco.

And because we cannot be sustained by bread alone:

“We follow in the bondage of Necessity. This is the bitterest pain to human beings: to know much and control nothing.”

Herodotus, Book 9, The Persian Wars