Since our last commentary in this series, several things have taken place. Let’s recall some of them: Jobs growth (based on January’s number) was much stronger than expected; inflationary pressures exhibited elevated numbers; the economy’s resilience became more evident; theories of a no landing scenario start circulating; fears that central banks will keep raising rates prevailed in the markets; yields rose; mortgage rates in the US surpassed the 7% level; and the equities markets erased a good chunk of previous gains.

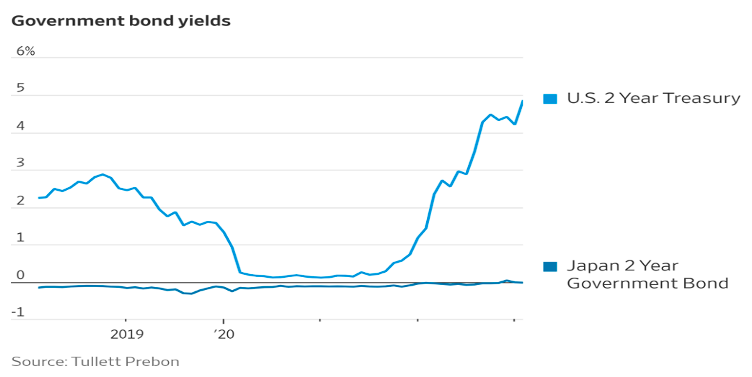

In an effort to cut the noise, allow us to share some graphs which are related to the topics above and present our thoughts. Let’s start with yields. As the first graph shows below, investors can park cash in 6-month Treasuries and gain 5%. That rich yield, which is way higher than the dividend yield earned from equities, is by itself attractive and we believe that yields will remain high for a longer period than anticipated, which helps conservative portfolios, keeps US assets and the greenback attractive, and allows for the financing of deficits.

The fact the 2-year Treasury Note yield also approaches 5% takes some refinancing risks (when the 6-month Treasuries mature) out of the equation and achieves financial and geopolitical goals.

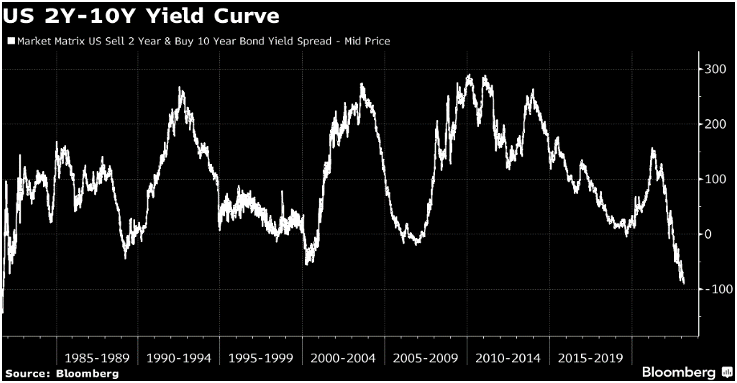

We have been hearing a lot about the inverted yield curve and the fact that 2-year Treasury Notes pay more than 10-year Treasury Bonds (see next graph). The inversion usually implies a forthcoming recession. We continue having reservations about this (i.e. no landing scenario) given the structural changes that are taking place in the economy (retirements, savings that serve as cushions for spending, energy transition, Putin’s and Xi’s war in Ukraine, strong jobs number, a revitalized service sector, inflation, and economic activity headed in the right direction as discussed below, supply chain corrections, new spending on the energy transition, tech innovations, no immediate refinancing pressure even for junk bonds, ability to adjust business plans and execution in the face of higher rates, and other changes).

The Fed and the European Central Bank (ECB) flooded the markets with cash in 2020 and 2021 and they were too late in raising rates in late 2022. Moreover, when they started raising rates, after missing the inflation boat, they were not believers in the fight. However, their recent over-zealousness in fighting inflation may be misplaced, as the graphs that follow show. Moreover, if we accept the fact that we can live with an inflation target of 3% given the structural changes in the economy, as well as the reality that even if the latter is rejected the 2% target is unachievable in 2023, then we can embrace the economic realism that says that rates need to stay higher longer than previous economic cycles, and that price targets can be achieved over a longer period of time. This will help the fixed-income market as well as advance stability in all markets (including materials, services, etc.) as a form of predictability will return, in the face of escalating geopolitical tensions.

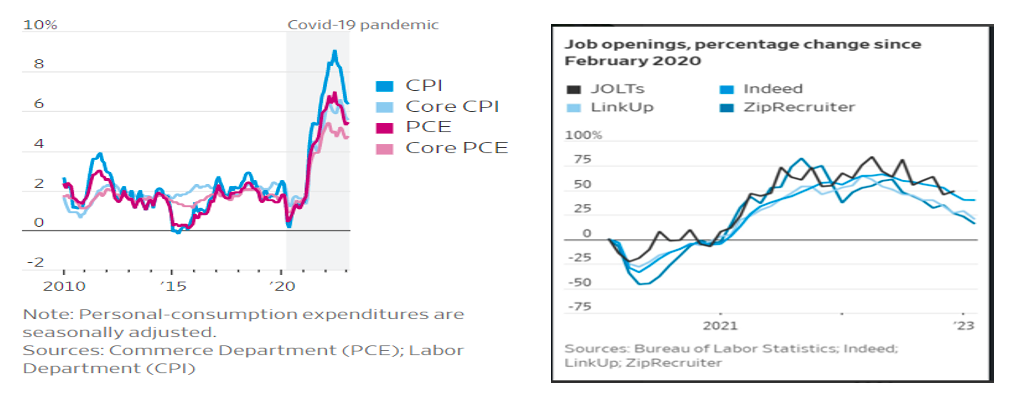

As shown below, all measures of inflation are on the right (disinflationary) track. Moreover, job openings and hirings are slowing down as the graph on the right demonstrates.

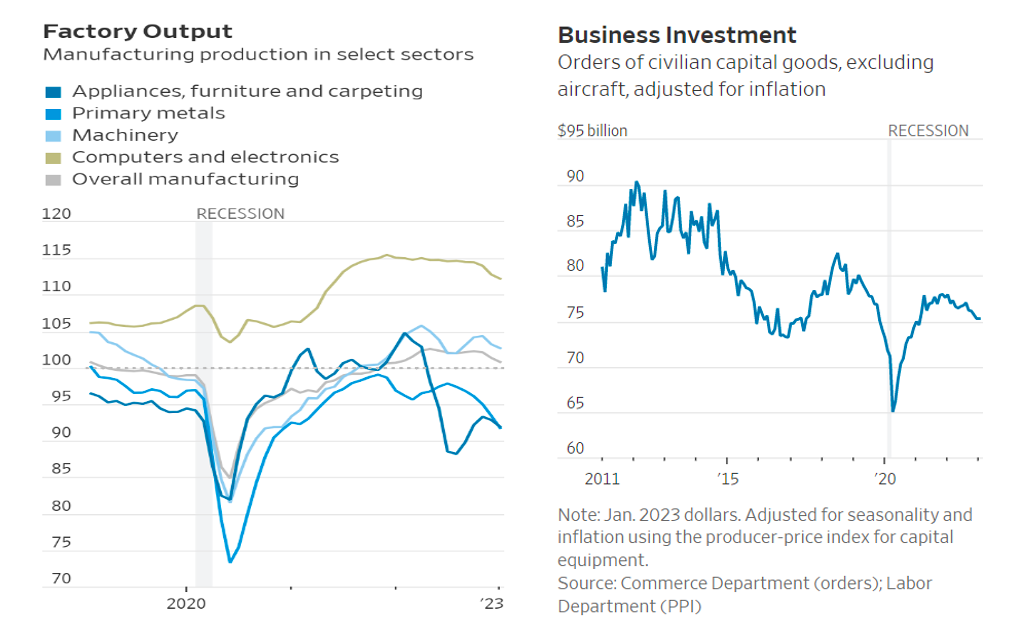

Finally, as also shown below, economic activity shows signs of interest rate compliance, as output slows down while investment spending follows the same path. Therefore, the effects of higher rates are taking place, but require more time in the face of an economic metamorphosis. It is our hope that the rate-setters (it remains always a case study that in a free economy a central authority is setting the price of money) will see the trajectory and allow markets room to breathe, and equilibrium to return.

And because we cannot be sustained by bread alone:

“Doomsday thinking offers no spark of hope; instead, it downs out all hope. As such it is one of the most dangerous deceptions of our time.” Bob Goudzwaard, in Idols of Our Time