Are the markets sending signals that run contrary to downbeat expectations? The latter includes IMF estimates for a global slowdown accompanied by recessions around the world, announced layoffs, lower earnings, accumulated disappointments due to losses in both stocks and bonds last year, geopolitical tensions and a war in Europe, inflationary pressures, market volatility, supply chain problems, higher interest rates and tighter monetary conditions, and declining business and consumer confidence, among others.

Let’s review some recent indicators:

- Inflation seems to be slowing down.

- From a historical standpoint, the decline in yields points to a decline in central banks’ rate increases; moreover, the size of those declines cannot preclude a cut in rates by the Fed and other central banks later in the year, if the economic pressures (signaling recession) intensify.

- China is reopening and thus demand should rise, supply constraints should loosen up, and some normalcy in Asian markets should return.

- The effects of sanctions on the Russian economy keep exercising economic pressure locally at a time when its invasion is not going the way that Putin wished for, and consequently, some rays of hope that the war in Ukraine may be ending by this spring are appearing on the horizon, especially if Putin realizes the threat of a Russian implosion.

- US and EU markets (equities and bonds) are exhibiting some early signs of strength.

- Oil demand is set to reach record highs (China’s reopening contributes significantly to that), which is a sign of healthy economic activity.

- The market’s breadth (rising vs. declining stocks) is rising, which is generally a healthy signal.

We could cite additional positive signals and indicators, but our purpose is to focus on what really matters. Therefore, while all of the above signals are positive, we remain cautious as optimism may be misplaced. The fact is that retail sales are dropping, industrial production is declining, corporate and consumer confidence remains restrained, Fed officials indicate that rates will reach 5.25-5.50% this year (from the current level of 4.25-4.50%), geopolitical tensions are not subsiding yet, rogue actors show no signs of limiting their malevolent plans, corporate earnings show clear signs of significant slowdown along with overall economic activity, real disposable income (after subtracting for inflation) is declining pointing to a slowdown in spending, and layoffs are being announced. Furthermore, debts are rising, hidden debts remain a problem, opaque valuations are plentiful, and at the current pace – unless yields drop significantly – the interest on US debt will exceed $1 trillion in the not-so-distant future.

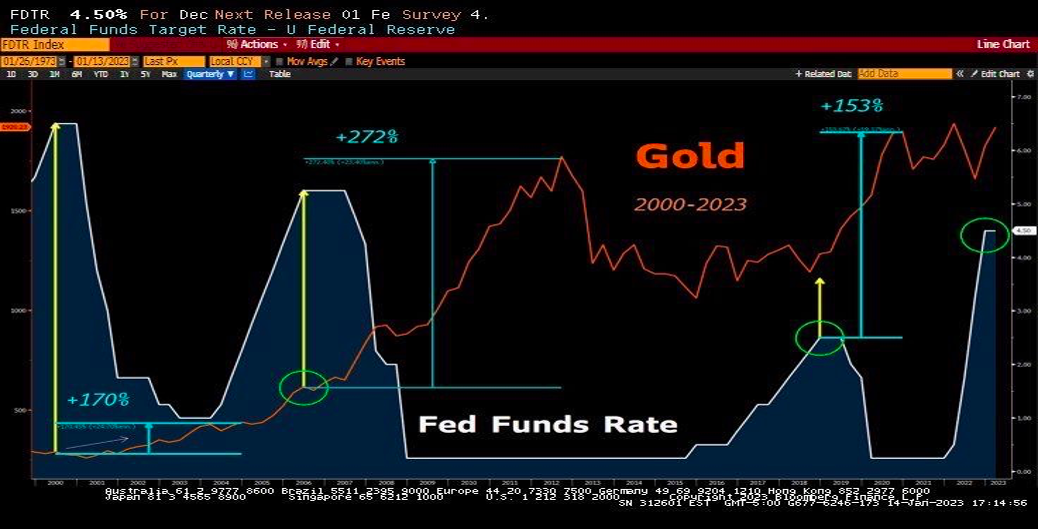

Where then do all those mixed signals leave us regarding portfolios and asset allocation? As we have indicated before, the energy sector remains strong and is expected to continue doing well. Investing in short-term Treasuries (1-12 months) that pay between 4.40-4.80% is a good option for cash, but the rei-investment risk remains (at the time of maturity investors may be unable to find similar rates), thus some increase in maturity might be wise (2-year Treasuries currently pay 4%). In addition, bond prices are positioned to make gains this year, so increasing the exposure to bonds overall may be prudent. Finally, and given the geopolitical tensions, some exposure to precious metals (if not already part of the portfolio) might be good as precious metals cannot be printed and, historically, they appreciate when central banks stop raising rates, as shown below.

And because we cannot live by bread alone:

“The study of history is …the only method of learning to bear with dignity the vicissitudes of fortune” – Polybius (200-118 BCE)