While we do not live in a world and a marketplace where the illusion that everything is fine and dandy dominates, an epidemic of denial as to the causes is prevalent and is sweeping the world and the markets. A wrong diagnosis will inevitably lead to the wrong treatment; that’s why addressing the cause and not the symptoms (such as inflation) is so important. Could the cause be fear – even terror – of losing a subliminal delusion? The rose-colored spectacles that we created by building empires of debt via unnatural interest rates and the rehypothecation mechanism might be looking for the establishment of a slaughterhouse where winners and speculators are being fed by the agonies/losses of others. Having said that, the economic fundamentals reject a market crash hypothesis, as explained at the end of this commentary.

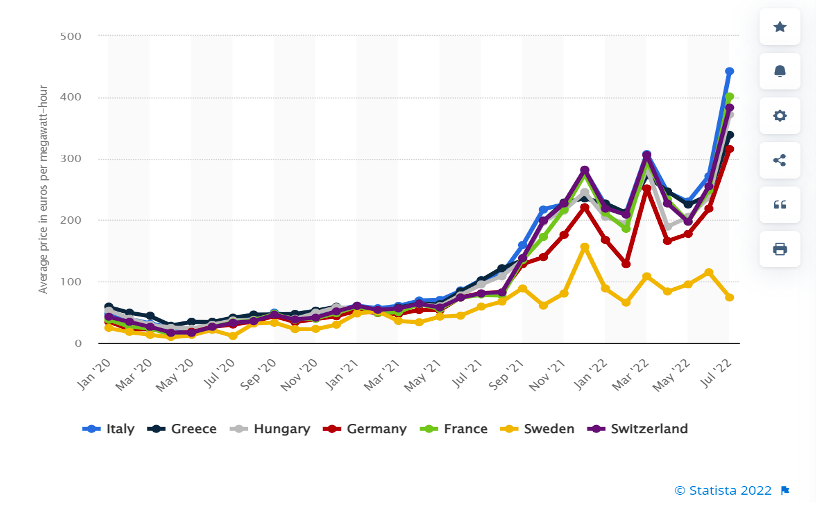

European power producers – despite the fact that are selling at record prices – may be facing a liquidity crisis due to rising collateral requirements in their hedging positions. Urgent measures are contemplated while inflationary pressures remain high. Budgets are being squeezed due to higher energy prices (see graph below), real purchasing power is declining, factories are closing, the dysfunctional fiat euro is at parity with the dollar (and possibly on a downward trajectory) while the sterling sits at 37-year low against the greenback.

When we turn our eyes to China, the reality is pretty worrisome: Industrial output is dropping, retail sales are declining, youth unemployment has reached 20%, investments are slowing down, manufacturing is contracting, and the Damoclean sword of debt (especially the one related to the real estate sector) is contributing to the 50% drop in GDP growth. Speaking of real estate in China, we need to remember that not only is it one of the most significant growth factors, but it also – according to Lombard Bank estimates – accounts for 70% of household wealth, 60% of local government, and 40% of bank lending. Needless of course to mention are the rising non-performing loans and the Chinese banking problems. However, China’s slowdown and its repressive regime with its failing policies amount also to being a major contributor to supply and demand issues and hence to the spreading misery.

We built a myopic world of Russian (especially for European energy) and Chinese dependence, and no one stands up to take responsibility for that. No wonder extreme movements are threatening political, economic, and social stability (we should be watching the Italian elections in a few days). Lack of foresight, and especiallyaprosperity bought on credit extended by belligerent leaders always backfires and now the world pays the price. The evolving reality of the war in Ukraine makes us wonder if tactical nuclear weapons is the next phase, as Putin’s world is shaken up on the war-front as well as domestically, given that dissenting voices seem to be rising.

Turning our eyes and ears now to the US markets, this past week (when on average markets dropped by more than 5%) revealed three things: First, that the environment described above is conducive to inflationary pressures and hence the Fed’s one-way street to raise rates (real rates that take into account inflation are still negative); second, an economic slowdown is materializing which affects sales and earnings expectations while companies announce restraints (from layoffs to cutting down growth plans); third, the fact that the S&P 500 closed below its 200-day moving average (a possible indicator of trend direction) for over 110 straight trading sessions feeds into the cycle of economic fear which, in turn, restrains growth due to the rising uncertainty that the issues discussed above generate.

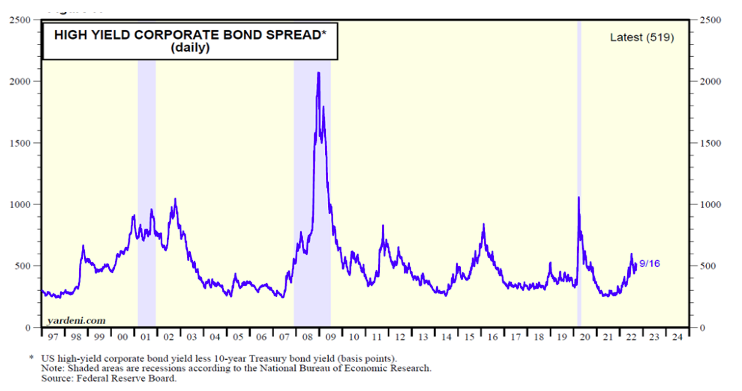

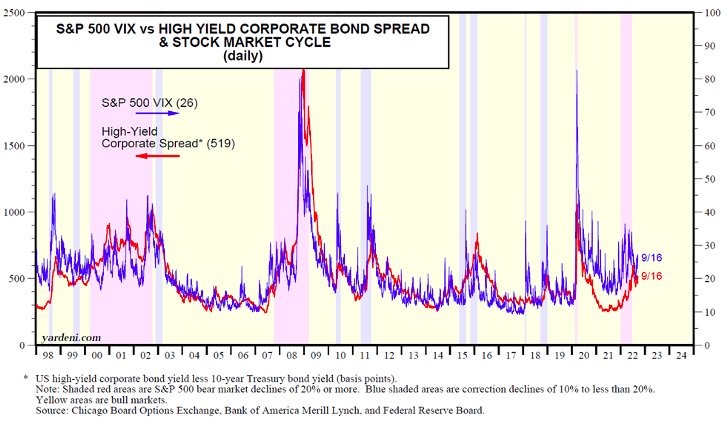

However, the fear of a market crash is exaggerated for three fundamental reasons: First, there is plenty of liquidity which is actually enhanced by capital inflows due to the strong dollar and the higher interest rate differentials. Second, corporate and household balance sheets (especially after the latter refinanced their debts at record low rates) are in much better shape than in previous downturns. Third, as shown below, the high yield spread (difference between high yield bonds and the 10-year Treasury) has increased but at a much moderate rate than previous slowdowns, while the VIX has remained subdued.

And because we cannot live by bread alone:

“While it’s true that someone can impede our actions, they can’t impede our intentions and our attitudes, which have the power of being conditional and adaptable. For the mind adapts and converts any obstacle to its action into a means of achieving it. That which is an impediment to action is turned to advance action. The obstacle on the path becomes the way.”

Marcus Aurelius, Meditations, 5.20