It’s time to look under the hood again and cancel the noise while trying to figure out what is happening. There are three issues we will be addressing in this commentary: Inflationary pressures, recessionary risks, and market trajectory.

Let us start with the latter. A number of headwinds seem to affirm our questioning of the recent market rally, namely: Inflationary pressures, recessionary threats, a “hawkish” Fed that has missed the boat, energy issues, tight labor markets, supply constraints, deglobalization risks, and, of course, geopolitical developments. The list is indicative of the downward pressures that the markets are facing. On the upside, liquidity is plentiful, incomes and savings remain strong, sales are equally strong, real interest rates are still negative, and earnings expectations point to forward earnings of around $225/share for the S&P 500, all of which are healthy signs. However, given the headwinds, market psychology could reverse course if some strong disappointments surface. We continue to be cautious, questioning market rallies and focusing on defensive sectors.

It’s not a coincidence that while equities are down by 8% on average, bonds are also down by more than 6%. Cash, of course, is losing its appeal given that its purchasing power has declined close to a double-digit figure (given that inflation on an annualized basis is already in double-digit territory). There are four main concerns that we have with inflation: First, it is broad-based where the share of items in the consumers’ basket that have been experiencing large price rises has been increasing steadily. Second, the expectation for even higher inflation becomes a self-fulfilling prophecy where businesses raise prices in anticipation of higher costs, and workers demand higher wages in anticipation of rising prices. Third, sensitive sectors, such as food and energy, are expected to keep experiencing rising prices. Fourth, tight supplies and logistical issues keep upward pressure on prices.

Bottom line: The Fed, which is primarily responsible for price stability, misjudged the facts, and with its transitory message, it failed to understand that this time the monetary base (a.k.a. high powered money) was being converted into money supply, therefore it failed to reverse the undercurrent threat at its root level. Hence, inflation is expected to remain elevated for the next several months.

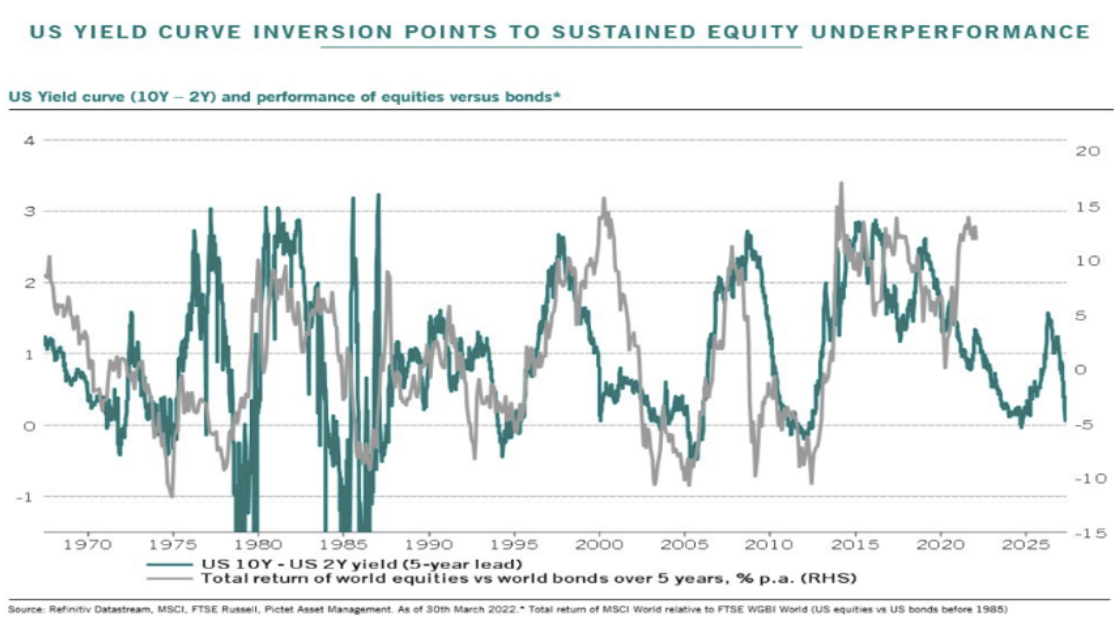

As the Fed is trying to play catchup, its hawkish tone points to rate increases of 50 bps in the next two meetings of the FOMC, as well as a reduction of its balance sheet (implying reduced market liquidity) by about $1.1 trillion in the next 12 months. Such a hawkish tone has contributed to rising Treasury yields, especially for Treasuries that mature in the next two years. Such increases have not only flattened the yield curve (decreasing the difference between short-term and long-term Treasury yields) but in some cases have contributed to a yield curve inversion (where, for example, a 2-year Treasury pays more than a 10-year Treasury). Historically, such inversions are associated with recessions. Moreover, the hawkish pivot by the Fed along with the high energy prices could become pivotal factors in reducing aggregate demand, which, in turn, could become the driving force in a recessionary scenario. Moreover, historically speaking, an inverted yield curve usually points to equity underperformance, as shown below.

Our current assessment regarding a recessionary scenario is that, in the next 6-10 months, the probability of a recession in the US is much lower (less than 10%) than the probability of a recession in the EU (over 25% and rising quite fast). There are four reasons for this: First, the energy impact is lower in the US than in the EU. Second, the upswing factors discussed earlier are stronger in the US. Third, real interest rates (once inflation is subtracted) are still negative (for both continents). Finally, as shown below, the percent of yield curves that have been inverted is relatively (to previous periods) small (a shaded area below represents a recessionary period). Having said that, we should clarify that if the headwinds prevail beyond November/December, the probability of a recession in both continents will increase significantly.

And because we don’t live by bread alone: