In this edition of our series, we are focusing on two fundamental questions:

- Is the market stabilizing given the new reality of growth and inflation?

- Why has Putin’s delusional madness not succeeded in conquering Ukraine despite Russia’s indisputable military superiority?

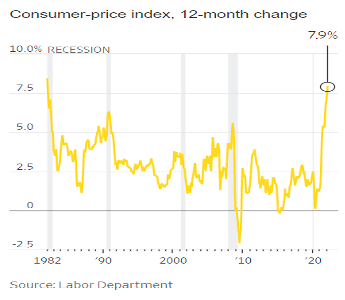

In an effort to provide a reasonable answer to the first question, we need first to digest the realities of growth and inflation. The following two figures reflect the inflationary landscape: It doesn’t look good, and it will be a great disappointment if the Fed fails us again (as it has been doing with its unreasonable easy-money policies and transitory propaganda) by not raising rates by at least 50 bps in the upcoming March meeting.

The ultra-accommodative monetary policy, the failure to anticipate inflation (especially after the fiscal expansionary policy of 2020-’22), the wage growth, the supply constraints, the higher aggregate demand, the disproportional price increases in crucial sectors, and the war in Ukraine, have all become a real threat to growth and real disposable income. The slowdown in growth, in combination with the slowdown in trade and China’s growth, could be reflected too in the graph below which simply tells us that the flattening of the spread between the 10 and 2-year Treasuries could spell trouble down the road.

Therefore, we believe that volatility (especially as it relates to the Ukrainian invasion) will remain high and we still recommend caution, plenty of cash, and hedging.

Now, regarding the second question, we believe that the kleptocratic regime in Russia simply embezzled the funds that were appropriated for the Russian military and, therefore, found itself unable to finish their unjust, immoral, and evil work in Ukraine in a manner that would have been expected. Money appropriated for the military was not used for military upgrades, and they got stuck by Ukraine’s resistance. Now, they would need to bring mercenaries from the Middle East to complete their work!