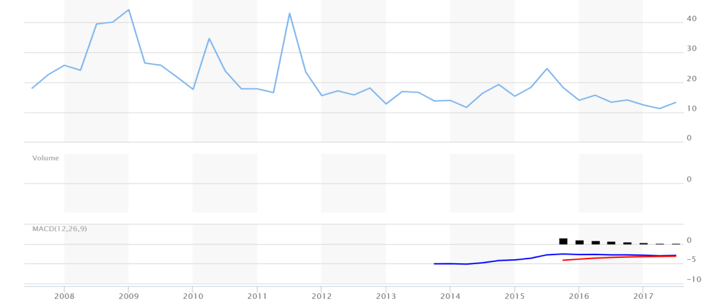

It has been well-recorded that the equity market’s volatility is pretty low by historical standards as the following 10-year graph shows. This kind of ataraxia (tranquility) may be the equivalent of the period when the Platonic and Aristotelian Schools of Thought were passing on the baton to the new Hellenistic era of philosophy when the epicenter of philosophical thinking was dominated by Epicureans, Stoics, and Sceptics.

The passing of the philosophical baton obliged philosophy to be appealing to a wider/cosmopolitan audience in Alexandria in Egypt, Pergamon in Asia Minor, Antioch in Syria and later Rhodes. Athens remained the capital of philosophy, but philosophy itself was changing. Philosophy now was seen as a guide to life and a source of comfort. Epicurus declared that “Empty are the words of that philosopher who offers no therapy for human suffering….There is no use in philosophy if it does not expel the suffering of the soul.”

The Hellenistic age of philosophy was dominated by Epicureans, Stoics, and Sceptics. If an Epicurean said one thing, the Stoic would say the opposite, and the Sceptic would not commit to either. However, they all agreed that philosophy had to be therapeutic. The new philosophers were popularizers. Such popularization of philosophy was distasteful to Cicero, who claimed that it was inconsequential.

In a similar manner, the markets are changing. The baton seems to be passing from a market that was guided by fundamentals, momentum, and emotions to a market guided by the visible hands of central banks, central government institutions/spending, and technological changes driven by just a few megacorps. The deployments of quantitative easing (QE) have brought an era of abnormal interest rates, given that nations (and possibly corporations and households given their historical high levels of debt) no longer can afford normal interest rates.

Socrates never spoke of ataraxia/tranquility being the aim of life. However, the new Schools of Thought (whether Epicurean, Stoic, or Sceptic) proclaimed that such was the purpose of life. The Epicureans’ objective was the defeat of fear. The persistence drop in the VIX index a.k.a. the fear index may reflect that Epicurean objective. The Stoic inquiry about living a life ‘in accordance with nature’ suggests the notion of a normal distribution a.k.a. reducing tail risks, i.e. making the SKEW index value as close to 100 as possible, implying that outlier risks are reduced or eliminated, and pointing to the implied volatility between writing puts (betting that the market is going down) and calls (betting that the market is going higher). It’s Epicureans vs. Stoics, and their battle brings ataraxia.

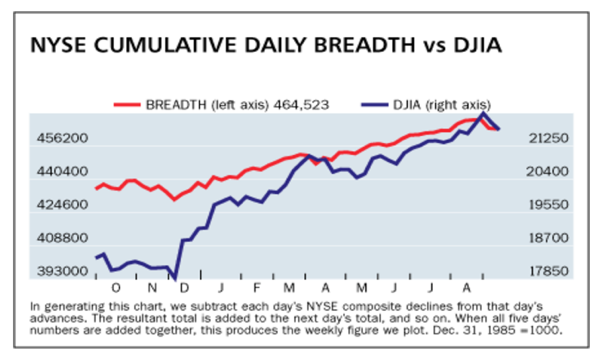

Finally the aim of the Sceptics – who believed that everything is determined by fate – was to suspend judgment, embrace resignation and acceptance, and make people stop worrying, i.e., yield themselves to the hands of fate. Ideally for Sceptics the market direction should be highly correlated to the market breadth (advancers minus decliners), as shown below.

Welcome to the world of random walkers and index investing. I am just wondering if the market inefficiencies will ever wake up the lethargy of those who believe that the safest place to be when the storm hits is the harbor.