Market Action

Compared to last week, global equities are expected to close modestly lower. The yield on the US 10-year Treasury note declined 6 basis points to 1.77% and the price of a barrel of West Texas Intermediate Crude oil rose $1.25 to $58.40. Volatility remained unchanged, as measured by the Chicago Board Options Exchange Volatility Index (VIX).

The US Congress passed a human rights bill this week to address the protests in Hong Kong, which have become increasingly violent over the last several months. The bill requires the US Secretary of State to certify that Hong Kong retains enough autonomy from China to qualify for special US trading considerations, recognizing its status as a world financial center. It also provides for sanctions against officials responsible for human rights violations in Hong Kong. The bill has provoked anger from mainland China, but US President Donald Trump is expected to sign the bill anyway. So far, the US and China have kept the issues in Hong Kong and trade negotiations separate, but there is a growing risk of the two issues becoming intertwined.

The United Kingdom’s current Prime Minister, Boris Johnson, and the Labour Party leader Jeremey Corbyn faced off in a debate this week in preparation for the general election scheduled for December 12th. This week’s opinion polls show that Johnson and his conservative party have a 14% lead. Markets are pricing with the expectation that Conservatives will be able to gain a majority in the House of Commons and therefore be able to pass a Brexit deal at the end of January.

The global manufacturing sector is continuing to show signs of stabilization. Data has improved in the US, Europe, and Japan this month with the exception of the United Kingdom whose manufacturing and services sector is contracting this month due to ongoing Brexit uncertainty.

Japan’s exports fell 9.2% in October while imports fell 14.8%. To offset the effects of the trade war and a recent tax consumption hike, the Japanese government announced it will implement a modest fiscal supplementary budget of 10 trillion yen ($9.2 billion).

What Could Affect the Markets in the Days and Weeks Ahead

Value shifting to the EU markets, might be observed in the first part of 2020.

EU markets are considered cheaper than US markets, hence a value shift in capital flows may be taking place in the weeks to come.

Chinese President Xi Jinping said this week that China wants to reach a “phase one” trade deal but that it will fight back when necessary. US President Donald Trump said this phase one deal is potentially “very close”. Chinese negotiators have invited the US to take part in face-to-face talks in Beijing. In addition, the US Department of Commerce issued a third 90-day extension for US firms to do business with Huawei.

Flash readings of eurozone inflation are due on November 29th. Predictions are for annual inflation to have edged up. Inflation rates in the eurozone have tracked with sentiment towards the US-China trade dispute this year. The European Central Bank’s President, Christine Lagarde, has pledged to review the bank’s inflation strategy.

This Week From BlackSummit

Recommended Read

Why Is South America In Turmoil? An Overview

What Markets Looked Like Just Ahead of Last Two Stock Downturns

France and Italy warned by Brussels over high debt levels

Physicists Just Created the Most Detailed Simulation of the Universe in History

Special Report: International Governance

Hong Kong is Xi Jinping’s failure

Perplexed by Brexit? Here Is a Guide

Video of the Week

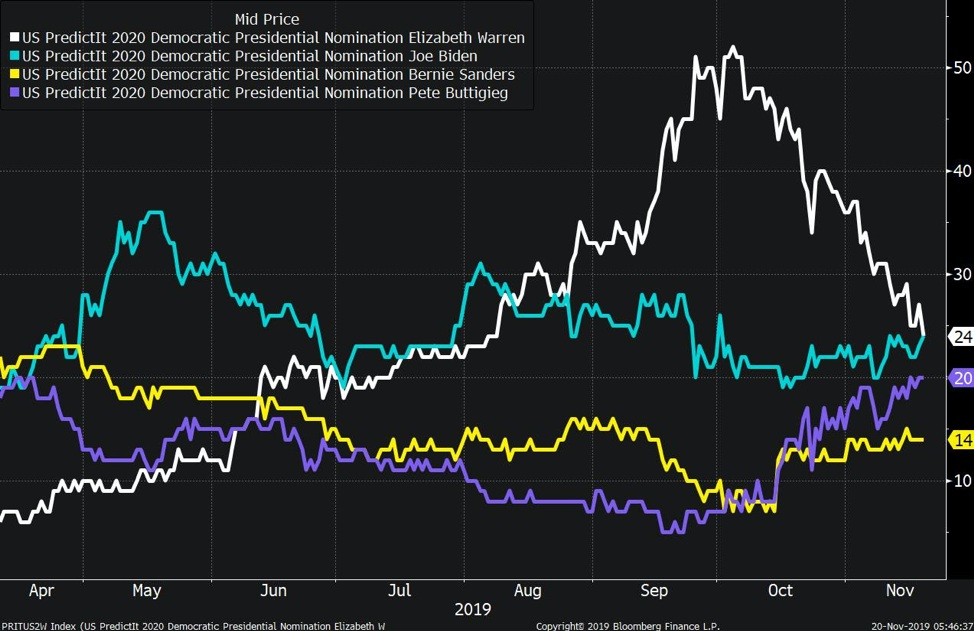

Image of the Week