Carbon Market News Roundup

Carbon Market News Roundup

-

Author : The BlackSummit Team

Date : July 19, 2024

| Volume 1, Issue 9 |

Welcome to our monthly newsletter, Carbon Market News Roundup, the goal of which is to introduce our audience to a new asset class market in the making: the carbon market. Our previous issues, along with the rest of our commentaries, may be read here.

In the last issue we explored recent guidelines for carbon markets that were handed down by the US government, and we finished our series on the electric vehicle market by focusing on emerging technologies that will be highly influential. This issue, we will review how the voluntary carbon market (VCM) has recently evolved, highlighting the significance of carbon removal technologies. We end this issue by examining the impact of climate change on the transition to renewable energy.

The Evolution of the Carbon Market: Carbon Removal Technologies

Is The Voluntary Carbon Market Moving Toward Version 2.0?

CarbonCredits.com

Carbon Removal Industry Reckons With a New Problem – Too Many Startups

Akshat Rathi, Bloomberg

Why Big Tech Is Pumping Big Money Into Companies Pulling CO2 From the Air

Jeff Young, Newsweek

The voluntary carbon market (VCM) is undergoing a significant transformation, driven by the pursuit of higher-quality credits and a surge in startups dedicated to carbon removal. Major corporations are increasingly investing in CO2 removal technologies, recognizing their potential to mitigate climate change. However, challenges remain, such as difficulty in sourcing high-quality credits and potential market oversaturation of carbon dioxide removal (CDR) startups.

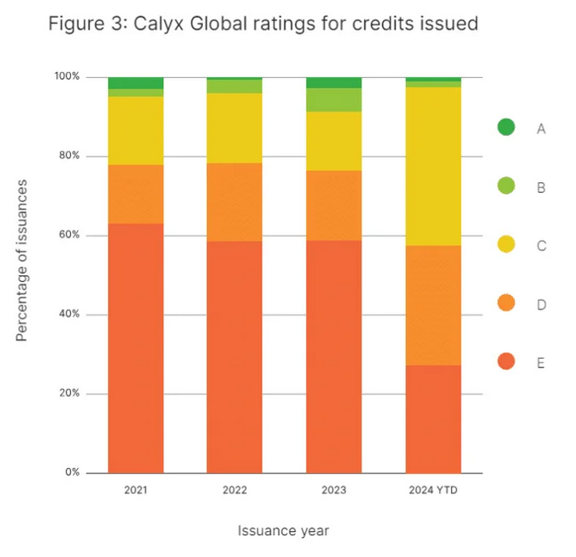

Since 2021, media scrutiny of the voluntary carbon market (VCM) has increased alongside a rise in carbon credit issuances, peaking in 2023. However, from early 2024, there has been a notable improvement in the quality of credit issuances.

Quality in the VCM varies significantly, with both poor and high-quality credits present in all sectors analyzed by Calyx Global, an independent carbon credit ratings platform. Over the past five years, only about 20% of credits rated fall into the top half of the rating scale (C+ and above), and less than 10% received a B rating or higher.

During 2024, the issuance of low-rated (E-rated) credits has dropped by nearly 50%, mainly due to a reduction in credits from REDD+ projects, which historically had lower ratings. This decline has been partially offset by an increase in credits from household and community projects, such as cookstove credits, which tend to have more C-rated credits.

Despite the overall improvement, high-rated credits (A and B ratings) remain rare due to the smaller number of such projects and their smaller scale compared to larger projects like REDD and large-scale renewable energy projects.

Phasing out low-quality credits will take time, as some are still tied up in forward contracts. While there have been improvements in rules and requirements for generating carbon credits, these updates need full integration into the active market.

Meanwhile, some of the highest-rated credits are ones that are issued from projects that remove CO2 from the atmosphere. Most carbon credits sold today are cheaper and focus on avoiding emissions rather than removing CO2. The voluntary nature of the carbon market incentivizes companies to buy the cheapest credits, not the most verifiable ones. This lack of demand for high-quality carbon removal has historically limited the number of startups.

However, now tech giants like Microsoft, Meta, Alphabet, and Salesforce are heavily investing in carbon dioxide removal (CDR) technologies to meet ambitious climate goals. These investments are crucial as these companies consume significant energy, especially with the rise of AI, which increases the demand for data centers and electricity.

Salesforce recently committed $25 million to the CDR investment company Frontier, emphasizing the need for early investment to ensure future availability of carbon removal technologies. While tech companies have previously invested in advanced carbon removal machinery, the pressure to decarbonize has intensified.

Source: Nat Bullard

The world needs about 5 billion tons of carbon removal per year by 2050, creating a potential $20 billion market by 2030. Now, there are over 800 startups dedicated to CDR. The market now faces an oversupply of startups and insufficient demand, a situation some see as a necessary phase to identify the most effective solutions. Despite this challenge, many believe that this is not a crisis, but instead the signs of an early market, one to be cultivated by a combination of both private investment and government incentives.

The Impact of Climate Change on Renewable Energy and Fossil Fuel Dependency

Carbon Emissions Hit a Record in 2023 Even as Renewables Soared, IEA Says

Will Mathis, Bloomberg

IEA Reveals Global CO2 Emissions Reach Record High in 2023, But Growth Slows

CarbonCredits.com

India’s climate crisis: New coal mining spreads as heat waves drain hydro dams

Priyanka Shankar & Valeria Mongelli, Nikkei

Despite the rapid growth in renewable energy, the paradox of rising carbon emissions continues to complicate efforts to combat climate change.

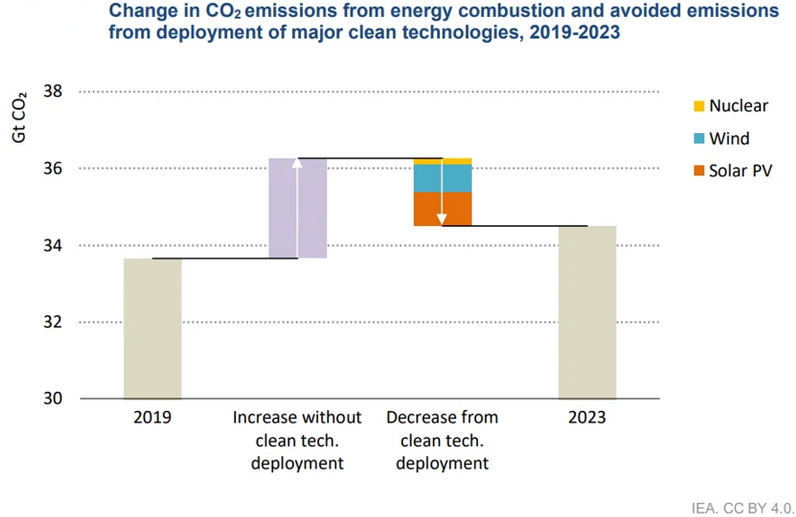

In 2023, despite a significant increase in renewable power production, global carbon dioxide emissions reached a new record high. Energy-related CO2 emissions rose by 1.1% to 37.4 billion metric tons, an increase of 410 million tons from the previous year. Extreme droughts, which reduced hydropower capacity in countries like China and the US, were a major factor in this rise. Climate change is expected to exacerbate droughts, further challenging hydropower reliability. However, wind, solar, and nuclear power are mitigating fossil fuel use. According to the International Energy Agency (IEA), without clean energy technologies, the rise in CO2 emissions over the past five years would have been three times larger.

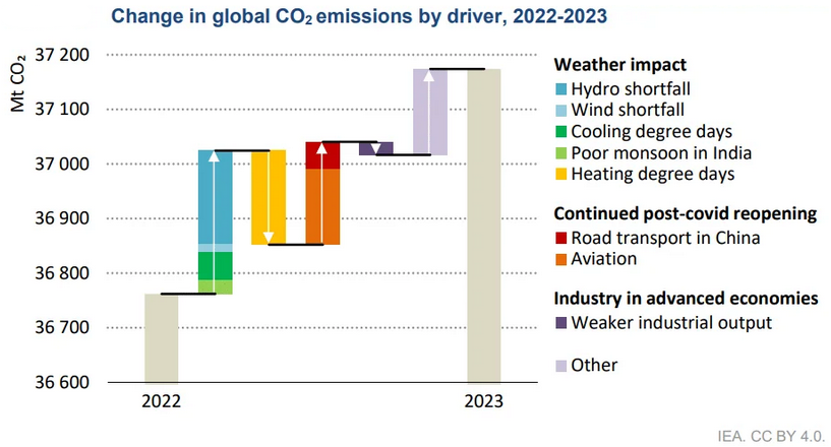

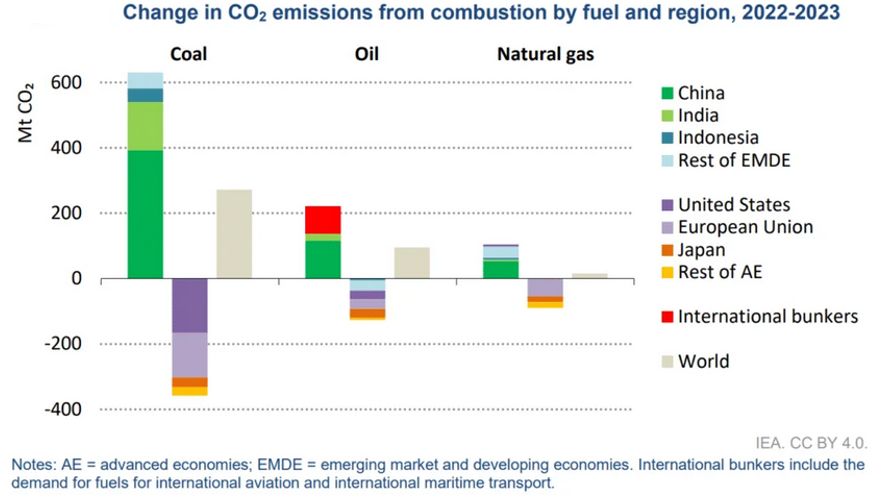

Moreover, droughts impaired the full operation of hydropower plants, necessitating a greater dependence on fossil fuels to satisfy energy needs. This shift accounted for nearly 40% of the total rise in emissions, as shown below.

Climate-induced events, such as droughts, further complicate the landscape by disrupting renewable energy production and reinforcing the ongoing reliance on fossil fuels. No more is this more illustrative than in India.

Hydropower’s share of India’s total power output fell to a record low of 8.3% in the fiscal year ending March 31, down from an average of 12.3% over the previous decade. Despite global moves away from fossil fuels, India continues to rely heavily on coal, which provides about 75% of its electricity, to support its economic development. Climate change has made monsoons more erratic, reducing hydroelectricity generation. This has led to increased coal mining, causing environmental and social unrest from communities near current and planned mines. While India has made significant strides in renewable energy, climate change is making hydro projects less reliable. The government aims to boost hydro capacity by over 50% by 2031-2032, but erratic weather patterns pose challenges. The transition to renewable energy is also hindered by higher transmission costs compared to coal.

Since the post-pandemic era, coal has emerged as the primary contributor to the surge in global CO2 emissions. Energy combustion emissions have witnessed a notable increase of around 850 million tonnes (Mt) since 2019, with coal emissions alone growing by 900 Mt.

Coal has accounted for around 70% of the upsurge in global carbon emissions from energy combustion in 2023. It contributes to around 270 Mt to the overall emission increase.

In the face of rising emissions, the greater use of coal despite the advances made in renewable energy show that progress is geographically uneven between the developed and developing world. Countries like India – those that have rapidly growing economies, populations, and are often the hardest-hit by the harmful effects of climate change – must find innovative solutions quickly in order to respond to this global problem.