Separating Sense from Nonsense in the Liquidity Debate

Separating Sense from Nonsense in the Liquidity Debate

-

Author : Joel Charalambakis

Date : June 18, 2015

The choir of voices sounding the alarm on market liquidity got a new member last week in the Wall Street Journal’s Op-Ed pages: Stephen Schwarzman of Blackstone, one of the largest financial services firms in the world and known for its leading role in private equity. Mr. Schwarzman points the finger at Dodd-Frank, the Volcker Rule, and capital regulations for reducing the market-making abilities of banks. With banks no longer a reliable presence, asset prices could violently fluctuate and instigate the next financial crisis, as the author argues.

The concerns over marketplace liquidity are very real in our eyes, as expressed in numerous commentaries prior to this. However, the reasoning and argument spelled out by Mr. Schwarzman distracts from a clear understanding on the state of the financial system and the means to guard against risks present and in the future.

It is accurate to state that banks have had to raise their capital levels and it is also true that the largest financial institutions have contracted their balance sheets in the wake of the Financial Crisis. However, the changes made have been marginal and more progress is needed to continue moving the sector in the right direction. Moreover, two events do not equate to cause and effect as laid out in the Op-Ed. Meeting the capital regulations can be done in two ways: raising equity (by selling shares or retaining earnings) or shrinking their asset claims. Banks have opted for the latter moreso than the former but that doesn’t impact the liquidity of asset markets. Using equity to acquire a home, for example, differs little from using debt, except, that is, when the market sours. Equity capital buffers against losses while debt does not. Thus, banks are not forced to sell assets, as Mr. Schwarzman argues, but rather are making a conscious choice to sell and stay out of markets because they want to minimize their use of equity.

The question is why have banks taken this route? Banks will argue that the cost of equity is prohibitive but that logic doesn’t hold as we explained in greater detail in our March newsletter (http://goo.gl/MYqBrR). Greater use of equity capital protects investors from downside risks, thus reducing the required return from equity. Moreover, if equity is so expensive why doesn’t it prohibit other large firms from using it while concurrently generating higher returns on investment (see table below from our March newsletter)

| Top 10 Banks By Assets | |||

| Company | Market Capitalization (Billions) | Debt/Equity Ratio | Return on Investment |

| JP Morgan | 231 | 1.31 | 6.60% |

| Bank of America | 168.31 | 1.08 | 7.60% |

| Citigroup | 162.49 | 1.12 | 8.10% |

| Wells Fargo | 282.55 | 1.11 | 9.10% |

| Goldman Sachs | 82.8 | 4.32 | 2.20% |

| Morgan Stanley | 69.3 | 4.34 | 1.80% |

| US Bancorp | 79.62 | 0.83 | 10.50% |

| BNY Mellon | 44.76 | 0.56 | 3.20% |

| PNC | 48.4 | 0.62 | 9.40% |

| Capital One | 43.51 | 0.67 | 16.10% |

| Top 10 Non-Financials in S&P 500 | |||

| Company | Market Capitalization (Billions) | Debt/Equity Ratio | Return on Investment |

| Apple | 736.31 | 0.30 | 26.20% |

| Exxon Mobil | 363.85 | 0.12 | 17.10% |

| Microsoft | 353.67 | 0.31 | 19.50% |

| Johnson & Johnson | 285.06 | 0.27 | 18.40% |

| Procter & Gamble | 228.54 | 0.55 | 11.70% |

| Pfizer | 217.18 | 0.48 | 8.70% |

| Verizon | 199.22 | 9.21 | 13.00% |

| Chevron | 196.91 | 0.18 | 6.40% |

| AT&T | 176.47 | 0.95 | 4.90% |

| 227.31 | 0.01 | 8.30% | |

The preference for debt has multiple factors, chief among them the fact that the interest payments on debt are tax deductible and that its use inflates IRR measures. Also to blame are compensation packages based upon Return on Equity metrics (which get inflated by high levels of debt) as well as Wall Street’s financial engineering of cash flows that vary in their liquidity and maturity profiles. Regardless, the reduced presence of banks in financial markets is reflective of a choice. Banks can have balance sheets as large as they wish so long as assets are financed with enough equity to comply with capital regulations. Whether those capital ratios are high enough to safeguard the system is another matter entirely.

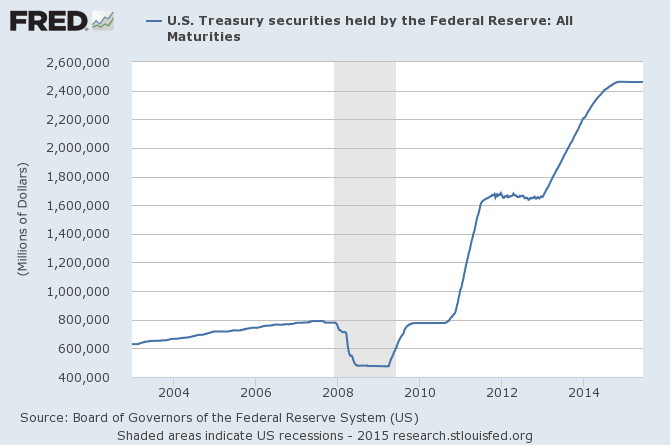

Finally, while the arguments included in the Op-Ed leave much to be desired, it is the material that is absent that sparks the most concern. Namely, the approximately $2 trillion in U.S. Treasury securities purchased by the Federal Reserve since 2009 (not to mention other securities) means that dealer institutions do not have the necessary collateral to clear derivative trades.

The implication emerging in the financial press that these liquidity issues wouldn’t be present if banks were allowed to act in their pre-crisis ways is folly. Banks, like other companies, are not servants of the markets but rather utilize markets to meet their own interests. They are not present to protect the public commons; if they were they wouldn’t have created the synthetic instruments that brought the global economy to its knees. Building a safer financial system should not involve envisioning banks as a bumper to falling asset prices.

To piggyback on Mr. Schwarzman’s metaphor, applying good medicine first requires the appropriate diagnosis. While the economy has in many ways recovered, the plumbing of the financial system is still fragile and susceptible to shocks. Addressing its weaknesses involves knowing where the risks are and are not present.