In its recent World Economic Outlook, the IMF questioned the sustainability of the current growth trajectory around the globe. This should not have been a surprise given the levels of unsustainable debts and liabilities around the world, as well as the fact that the banking sector (official and shadow, especially in China and Europe) with opaque and toxic instruments on its balance sheet cannot escape from a velocity that leads them not just into negative interest rates but even worse into a negative equilibrium.

Real interest rates have been negative for a long time. For the last 85 years the before-tax average rate of return on US T-bills was about 3.7 percent and the average inflation rate about 3 percent. Thus, ignoring taxes the real return was about 0.7 percent. However, assuming an average tax rate of 25 percent, the average after-tax real return was approximately -0.27%. The same thing can be concluded for long-term government bonds as well as for corporate bonds. Therefore, we have lived in a world of negative real interest rates for a long time.

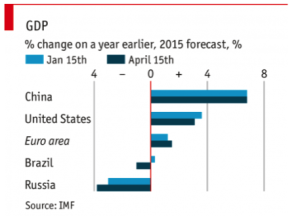

Let’s now see the growth trajectory as depicted in the IMF’s biannual assessment.

As the graph above shows, the growth prospects for the US have weakened due to a stronger dollar, lower investment spending (especially in the energy sector), and some weakness in corporate profits. Our assessment is that the latter will reverse in the second half of the year, foreign sales will stabilize, while lower investment spending will be offset by higher capital inflows, more lending, and higher consumer spending. Thus, overall we expect US growth to stay within the 3-3.3% range, and the equities markets to move from its current sideways mode into a positive territory, while bond prices to strengthen as yields may try to find a convergence path with EU-sovereign yields, exacerbating the negative history of the last 85 years.

European equity markets are expected to show greater potential as the ECB’s QE exercises continue and the Euro heads towards parity with the US dollar. The IMF has upgraded EU prospects, but even that does not put the dysfunctional EU into the healthy category. It’s a mirage and the ECB’s placebo therapy is enhancing the process of trying to create fools, given that the real problems are not being addressed.

Regarding Chinese prospects we would refer the reader to our previous commentary, and we would add that the latest developments seem to vindicate our view, (see http://stage.blacksummitfg.com/2950).

Allow me however to revisit the issue of secular stagnation (a condition of anemic growth in an environment of zero rates where savings glut conditions lead to declining incomes and weak currencies). As stated before, I find this concept a mythical reality in the sphere of propaganda that serves the purpose of kicking the can down the road in order to avoid the radical surgery that is needed to remove the cancerous cells of debt and credit overextension based on questionable assets. Interest rates have declined because of central bank activity. Such a decline can only make the situation worse, since it creates false expectations and dislocations by artificially appreciating assets and thus creating a black hole.

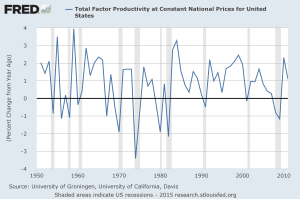

The declining growth rate in total factor productivity (see graph below) along with the slowdown in emerging economies (mainly China) are two ingredients whose mix creates an environment of negative equilibrium where growth turns negative when a major asset class bursts (such as the bond market, or the need to recapitalize all EU central banks because of a Greek default).

The implosion of a major asset bubble at a time when central banks’ schemes can no longer work, will dislocate supply and demand forces in all markets (goods, services, production, labor, commodities, financial, currencies, etc.). The proponents and silent supporters of the secular stagnation propaganda keep arguing about desired savings over investment levels (implying a disequilibrium in interest rates), however they fail to address the heart of the issue, which is the need for catharsis and creative destruction of unsustainable policies.

Until then, the fools will be fooled in the greater scheme of things where useful idiots advance the causes destined to wipe out paper wealth.

Negative Equilibrium: The Sustainability of the Unsustainable

Author : John E. Charalambakis

Date : April 22, 2015

In its recent World Economic Outlook, the IMF questioned the sustainability of the current growth trajectory around the globe. This should not have been a surprise given the levels of unsustainable debts and liabilities around the world, as well as the fact that the banking sector (official and shadow, especially in China and Europe) with opaque and toxic instruments on its balance sheet cannot escape from a velocity that leads them not just into negative interest rates but even worse into a negative equilibrium.

Real interest rates have been negative for a long time. For the last 85 years the before-tax average rate of return on US T-bills was about 3.7 percent and the average inflation rate about 3 percent. Thus, ignoring taxes the real return was about 0.7 percent. However, assuming an average tax rate of 25 percent, the average after-tax real return was approximately -0.27%. The same thing can be concluded for long-term government bonds as well as for corporate bonds. Therefore, we have lived in a world of negative real interest rates for a long time.

Let’s now see the growth trajectory as depicted in the IMF’s biannual assessment.

As the graph above shows, the growth prospects for the US have weakened due to a stronger dollar, lower investment spending (especially in the energy sector), and some weakness in corporate profits. Our assessment is that the latter will reverse in the second half of the year, foreign sales will stabilize, while lower investment spending will be offset by higher capital inflows, more lending, and higher consumer spending. Thus, overall we expect US growth to stay within the 3-3.3% range, and the equities markets to move from its current sideways mode into a positive territory, while bond prices to strengthen as yields may try to find a convergence path with EU-sovereign yields, exacerbating the negative history of the last 85 years.

European equity markets are expected to show greater potential as the ECB’s QE exercises continue and the Euro heads towards parity with the US dollar. The IMF has upgraded EU prospects, but even that does not put the dysfunctional EU into the healthy category. It’s a mirage and the ECB’s placebo therapy is enhancing the process of trying to create fools, given that the real problems are not being addressed.

Regarding Chinese prospects we would refer the reader to our previous commentary, and we would add that the latest developments seem to vindicate our view, (see http://stage.blacksummitfg.com/2950).

Allow me however to revisit the issue of secular stagnation (a condition of anemic growth in an environment of zero rates where savings glut conditions lead to declining incomes and weak currencies). As stated before, I find this concept a mythical reality in the sphere of propaganda that serves the purpose of kicking the can down the road in order to avoid the radical surgery that is needed to remove the cancerous cells of debt and credit overextension based on questionable assets. Interest rates have declined because of central bank activity. Such a decline can only make the situation worse, since it creates false expectations and dislocations by artificially appreciating assets and thus creating a black hole.

The declining growth rate in total factor productivity (see graph below) along with the slowdown in emerging economies (mainly China) are two ingredients whose mix creates an environment of negative equilibrium where growth turns negative when a major asset class bursts (such as the bond market, or the need to recapitalize all EU central banks because of a Greek default).

The implosion of a major asset bubble at a time when central banks’ schemes can no longer work, will dislocate supply and demand forces in all markets (goods, services, production, labor, commodities, financial, currencies, etc.). The proponents and silent supporters of the secular stagnation propaganda keep arguing about desired savings over investment levels (implying a disequilibrium in interest rates), however they fail to address the heart of the issue, which is the need for catharsis and creative destruction of unsustainable policies.

Until then, the fools will be fooled in the greater scheme of things where useful idiots advance the causes destined to wipe out paper wealth.