Since 1873 the world has suffered two periods of great deflationary pressures: the first one from 1873-1893, and the second during the Great Depression in the 1930s. We may be facing a third one (at least according to several analysts), which has been forcing the central banks around the world to unconventional measures of quantitative easing (QE) in order to stimulate inflation via unnatural repression of interest rates and the buying of bonds (mainly government securities). Needless to say that such unconventional measures may entail significant risks given that they neglect the structural causes of the problems reflected in a system that accumulates unsustainable debts and liabilities while lacking an anchor in the midst of uncharted waters.

Financial earthquakes can take place not only due to balance of payments problems but also whenever the level of available acceptable collateral dries up. The situation becomes more fragile whenever credit has been extended based on questionable (toxic) collateral, and it is even more troubling now that trillions of dollars are involved in derivative contracts. It is my opinion that equilibrium in these circumstances can only be achieved through a general deflation of debts, and any unnatural manipulation of the monetary base and of interest rates makes the inevitable bursting worse.

Let’s take a look at the ECB’s implementation of its QE program: As it buys bonds from banks and holds them on its balance sheet it will deprive the markets from valuable collateral. The funds that will be used to purchase those bonds will remain as reserves in the Eurosystem and will not be converted into money supply. The reduction of the collateral base due to the QE will reduce the velocity of collateral, which in turn will reduce money velocity in the EU especially given the fact that there is already too much debt and the base of qualified borrowers may be drying up. Hence, while the ECB changes its tactic from moral suasion to a step of action the expected outcome has the same trajectory as its moral suasion arguments i.e. to just lift up hopes and kick the can down the road without addressing the real issues and causes of the crisis. As for the celebrated pronouncements that the EU economy has turned the corner and it is on its path to a meaningful recovery due to 0.3% growth in the last quarter, I could only say that it is wishful thinking.

The depreciation of the Euro is significant as the following graph shows, however this will not suffice because EU products will need to compete with Chinese and Japanese goods in an era when both of them are cheapening their currencies in order to stimulate exports and growth. At the same time, demand for credit may be slowing due to the inability of the EU to generate growth as well as due to over-indebtedness.

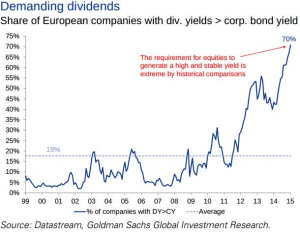

The fact that yields for EU bonds are so low and the interest-rate/yield differentials with the US grow will force capital flight away from the EU that may dry up capital markets. This latter point brings me to another issue which seems to have been neglected in the mainstream publications. As the following graph show, about 70% of EU companies pay a dividend yield that exceeds the corporate bond rate. This introduces malfunctions in the capital markets because it’s a carrot for companies to call in the existing bonds and issue new ones at lower rates. This reinvestment risk has been downplayed, but it should not, because it represents an artificial boost to equities’ valuations, leading them to bubble territory.

However, this is not just an EU phenomenon. As the following table shows, well-known US names have dividend yields that far exceed any normal risk premium.

| Company |

Dividend Yield % (6/30/14) |

5-Year Bond Yield % (6/30/14) |

| AT&T |

5.20 |

2.08 |

| Chevron |

3.28 |

1.79 |

| Cisco |

3.06 |

2.31 |

| General Electric |

3.35 |

1.84 |

| Intel |

2.91 |

2.78 |

| McDonalds |

3.22 |

1.85 |

| Merck |

3.04 |

1.95 |

| Pfizer |

3.50 |

1.95 |

| Procter & Gamble |

3.28 |

1.77 |

| Verizon |

4.33 |

2.21 |

| Average |

3.73 |

2.23 |

The combination of an environment where collateral dries up, unnatural yields prevail, the recycling of petrodollars is reduced, debts are unsustainable, and the Chinese economy experiences a significant slowdown, may point out to an emerging divergence between the real and the financial economy which advances economic uncertainty and increases portfolio risks.

Drying Up The Collateral Base

Author : John E. Charalambakis

Date : March 11, 2015

Since 1873 the world has suffered two periods of great deflationary pressures: the first one from 1873-1893, and the second during the Great Depression in the 1930s. We may be facing a third one (at least according to several analysts), which has been forcing the central banks around the world to unconventional measures of quantitative easing (QE) in order to stimulate inflation via unnatural repression of interest rates and the buying of bonds (mainly government securities). Needless to say that such unconventional measures may entail significant risks given that they neglect the structural causes of the problems reflected in a system that accumulates unsustainable debts and liabilities while lacking an anchor in the midst of uncharted waters.

Financial earthquakes can take place not only due to balance of payments problems but also whenever the level of available acceptable collateral dries up. The situation becomes more fragile whenever credit has been extended based on questionable (toxic) collateral, and it is even more troubling now that trillions of dollars are involved in derivative contracts. It is my opinion that equilibrium in these circumstances can only be achieved through a general deflation of debts, and any unnatural manipulation of the monetary base and of interest rates makes the inevitable bursting worse.

Let’s take a look at the ECB’s implementation of its QE program: As it buys bonds from banks and holds them on its balance sheet it will deprive the markets from valuable collateral. The funds that will be used to purchase those bonds will remain as reserves in the Eurosystem and will not be converted into money supply. The reduction of the collateral base due to the QE will reduce the velocity of collateral, which in turn will reduce money velocity in the EU especially given the fact that there is already too much debt and the base of qualified borrowers may be drying up. Hence, while the ECB changes its tactic from moral suasion to a step of action the expected outcome has the same trajectory as its moral suasion arguments i.e. to just lift up hopes and kick the can down the road without addressing the real issues and causes of the crisis. As for the celebrated pronouncements that the EU economy has turned the corner and it is on its path to a meaningful recovery due to 0.3% growth in the last quarter, I could only say that it is wishful thinking.

The depreciation of the Euro is significant as the following graph shows, however this will not suffice because EU products will need to compete with Chinese and Japanese goods in an era when both of them are cheapening their currencies in order to stimulate exports and growth. At the same time, demand for credit may be slowing due to the inability of the EU to generate growth as well as due to over-indebtedness.

The fact that yields for EU bonds are so low and the interest-rate/yield differentials with the US grow will force capital flight away from the EU that may dry up capital markets. This latter point brings me to another issue which seems to have been neglected in the mainstream publications. As the following graph show, about 70% of EU companies pay a dividend yield that exceeds the corporate bond rate. This introduces malfunctions in the capital markets because it’s a carrot for companies to call in the existing bonds and issue new ones at lower rates. This reinvestment risk has been downplayed, but it should not, because it represents an artificial boost to equities’ valuations, leading them to bubble territory.

However, this is not just an EU phenomenon. As the following table shows, well-known US names have dividend yields that far exceed any normal risk premium.

The combination of an environment where collateral dries up, unnatural yields prevail, the recycling of petrodollars is reduced, debts are unsustainable, and the Chinese economy experiences a significant slowdown, may point out to an emerging divergence between the real and the financial economy which advances economic uncertainty and increases portfolio risks.