Bob Dylan’s song “The times they ‘re a changing”, fits pretty well in today’s global picture. The landscape is changing indeed. Where should we start?

- In the Arab world?

- In the fiscal imbalances in the EU but also in the US?

- In the credit mechanism and its collateral basis?

- In the way that monetary policy is being conducted?

- In the rising role of developing and emerging markets?

- In the descent of currencies and fiat money?

- Or is it time to ask again, “Who Killed Homer?” and the classical education paradigm that has resulted in minds’ compartmentalization that cannot separate education from training?

We wrote last week that we expect oil prices to rise, and boy has it! On average each of our portfolios holds at least 15% in energy-related securities. While the turmoil continues in the Arab world, and the road is being prepared for the Day After (part of the new Silk Road we have been writing about), commentators are pointing out that investors did not seek the safety of the dollar during these days, but rather sought after precious metals, hinting that the dollar may have started its descent even in times of crisis. While we are thrilled that people start viewing precious metals as money, we believe that the greenback’s movements strengthen the US position.

Our contrarian view says that it is great for the US and its recovery that the dollar did not strengthen during this crisis. Such a non-event, actually strengthens the US recovery and hence advances the chances for a smoother recovery for the rest of the developed world, too. That of course, does not mean that a strengthening of the dollar will not take place. It will probably happen, given the fact that the Euro is overvalued at current levels, and that the March 24-25 EU summit may prove to be another indecisive gathering of weak leaders who are unable to make necessary decisions that exhibit leadership, vision, and strategic thinking. In that case, the dollar will strengthen due to the weakness of the Euro. Moreover, a strengthening of the dollar at a time of oil increases, reduces the recovery efforts of developed countries such as UK, Portugal, and Japan, all of which saw their GDP to decline for the last quarter of 2010, potentially hinting to a double dip in those economies.

Our position is that the dollar’s non-appreciation makes US external position stronger, in a similar manner that the dollar’s depreciation during the 2007-’09 crisis improved its external position by at least $450 billion. Let us also not forget that the overall indebtedness does not change since the debt is owed in US dollars. On the contrary, foreign holdings are improving when non-appreciation takes place. Hence, during this Arab crisis, the US is positioning herself in the best possible way, while its geostrategic and geoeconomic positions look better than expected, given the historic changes that will advance growth and opportunities in a similar manner that growth and opportunities were advanced with the fall of the iron curtain, and it seems that this time around the assets behind the changing landscape might be even better.

Moreover, let’s not forget that we live in an era where deflationary forces in the developed world are combined with inflationary pressures in the developing and emerging markets, and this divergence cannot coincide with the dollar’s appreciation. Thus, the non-appreciation of the greenback probably advances the chances of a continuous recovery.

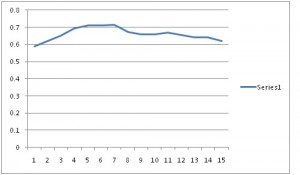

The figure below shows the US dollar share of global reserves in the last 15 years. As you can see, the share of the dollar has not changed significantly during those years, and actually by the end of 2009 it was a bit higher than it was in 1995. We are of the opinion that its share will increase in the foreseeable future (for reasons explained earlier i.e. the changing landscape), and that the US greenback will strengthen its role, especially if inflationary pressures keep building up in developing markets.

Source: IMF Statistics on Currency Composition of Official Foreign Exchange Reserves (COFER)

Ode to exits via the New Silk Road!

A Treacherous Rebalancing Act: A Currency View

Author : John E. Charalambakis

Date : March 2, 2011

Bob Dylan’s song “The times they ‘re a changing”, fits pretty well in today’s global picture. The landscape is changing indeed. Where should we start?

We wrote last week that we expect oil prices to rise, and boy has it! On average each of our portfolios holds at least 15% in energy-related securities. While the turmoil continues in the Arab world, and the road is being prepared for the Day After (part of the new Silk Road we have been writing about), commentators are pointing out that investors did not seek the safety of the dollar during these days, but rather sought after precious metals, hinting that the dollar may have started its descent even in times of crisis. While we are thrilled that people start viewing precious metals as money, we believe that the greenback’s movements strengthen the US position.

Our contrarian view says that it is great for the US and its recovery that the dollar did not strengthen during this crisis. Such a non-event, actually strengthens the US recovery and hence advances the chances for a smoother recovery for the rest of the developed world, too. That of course, does not mean that a strengthening of the dollar will not take place. It will probably happen, given the fact that the Euro is overvalued at current levels, and that the March 24-25 EU summit may prove to be another indecisive gathering of weak leaders who are unable to make necessary decisions that exhibit leadership, vision, and strategic thinking. In that case, the dollar will strengthen due to the weakness of the Euro. Moreover, a strengthening of the dollar at a time of oil increases, reduces the recovery efforts of developed countries such as UK, Portugal, and Japan, all of which saw their GDP to decline for the last quarter of 2010, potentially hinting to a double dip in those economies.

Our position is that the dollar’s non-appreciation makes US external position stronger, in a similar manner that the dollar’s depreciation during the 2007-’09 crisis improved its external position by at least $450 billion. Let us also not forget that the overall indebtedness does not change since the debt is owed in US dollars. On the contrary, foreign holdings are improving when non-appreciation takes place. Hence, during this Arab crisis, the US is positioning herself in the best possible way, while its geostrategic and geoeconomic positions look better than expected, given the historic changes that will advance growth and opportunities in a similar manner that growth and opportunities were advanced with the fall of the iron curtain, and it seems that this time around the assets behind the changing landscape might be even better.

Moreover, let’s not forget that we live in an era where deflationary forces in the developed world are combined with inflationary pressures in the developing and emerging markets, and this divergence cannot coincide with the dollar’s appreciation. Thus, the non-appreciation of the greenback probably advances the chances of a continuous recovery.

The figure below shows the US dollar share of global reserves in the last 15 years. As you can see, the share of the dollar has not changed significantly during those years, and actually by the end of 2009 it was a bit higher than it was in 1995. We are of the opinion that its share will increase in the foreseeable future (for reasons explained earlier i.e. the changing landscape), and that the US greenback will strengthen its role, especially if inflationary pressures keep building up in developing markets.

Source: IMF Statistics on Currency Composition of Official Foreign Exchange Reserves (COFER)

Ode to exits via the New Silk Road!